Feltrin: “The sector has sailed through the storm better than others. Exports held up and closed at -2.3%. A strategic show more than ever”.

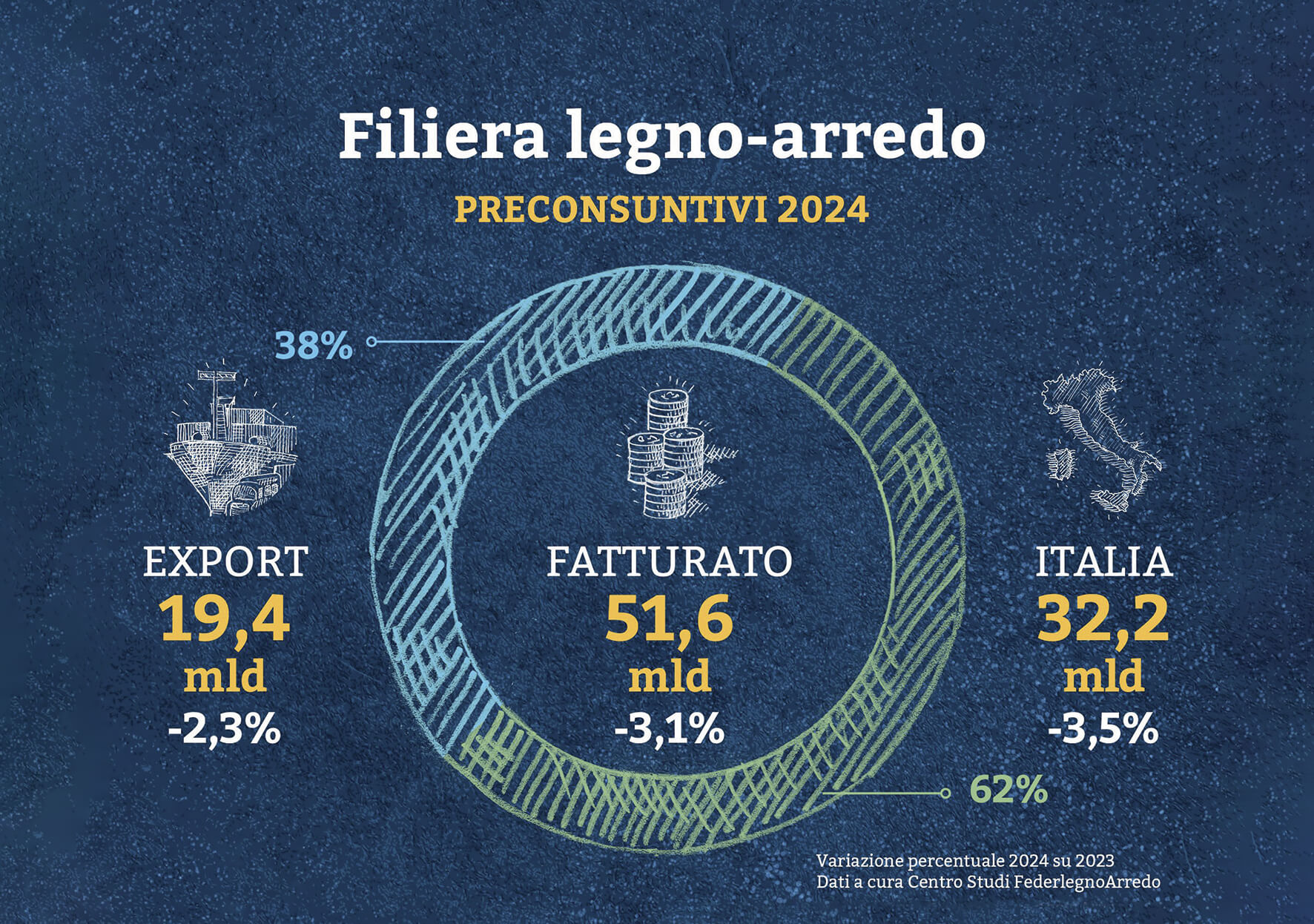

The wood-furniture supply chain closes in 2024 with a production turnover of 51.6 billion euros, down 3.1% (53.2 billion in 2023), in continuity with the normalization that began in 2023, after two years of growth for the sector. That is according to the preliminary figures processed by the FederlegnoArredo Study Centre on Istat data. A decline that concerns sales on the domestic market equal to 32.2 billion euros, which constitutes over 60% of the total turnover and record a -3.5%, due to the reduction of tax incentives provided in previous years. Exports, which represent 38% of the total turnover of the supply chain, closed at -2.3% with a value of 19.4 billion euros. The trade balance of the supply chain is close to 8 billion euros (it was 8.4 billion in 2023).

“A drop of 3.1% – comments the president of FederlegnoArredo, Claudio Feltrin – is still to be considered contained given the current economic and geopolitical context and compared to what we could expect. This does not mean that the situation is easy, but the contrary. Anyway, we can say that – as in other times – the supply chain has navigated better than others, even in very stormy waters.

Proof of that is the data on industrial production in ’24, which differs little from that of 2019, confirming the stability in numbers and the increasingly high predisposition of the public to recognize the value of the products of our design, which has always been synonymous with quality, innovation and style. However, we have no illusions. We are aware of how much the fragile balances across the border, the economic crises in Germany and France, and the possible entry of Chinese products into our markets as a result of the feared introduction of American duties, are variables that will put a strain on companies in the first months of 2025,” continues Feltrin.

“They will have to quickly identify alternative outlet markets and plan strategic investments even in terms of sustainability, training for the digital transition and alternative forms of energy supply, the costs of which have returned to have a strong impact on companies’ budgets. Industrial production in November recorded +3.6% even if the cumulative remains negative (-2.8%). Therefore, it is difficult to make long-term predictions, but one thing is certain: despite this situation, companies have strengthened their confidence in the Salone del Mobile.Milano 2025 as a strategic opportunity: exhibiting in the pavilions of Rho Fiera is the most powerful access key for business in the sector. Now more than ever, there is a need for the Salone del Mobile“.

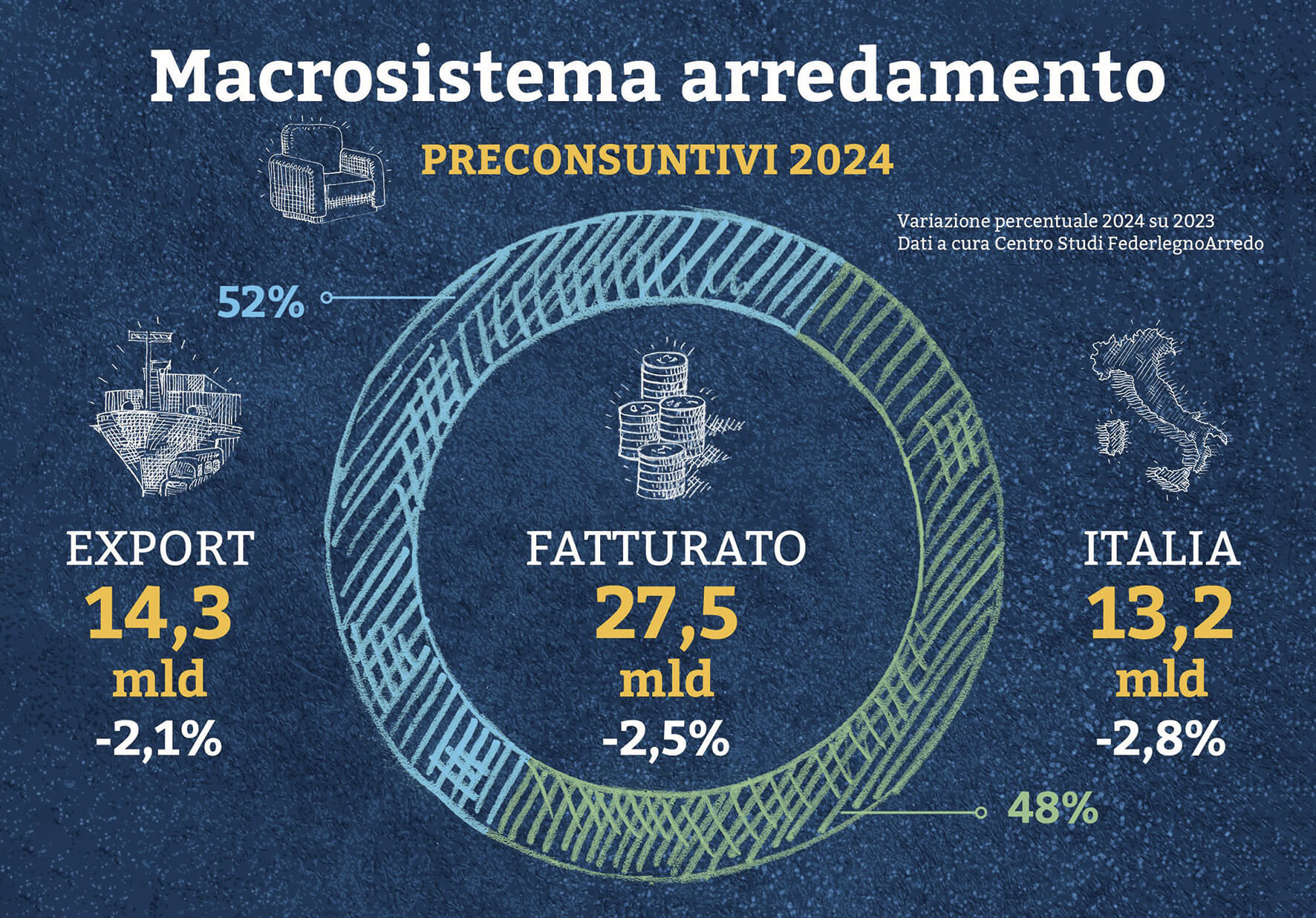

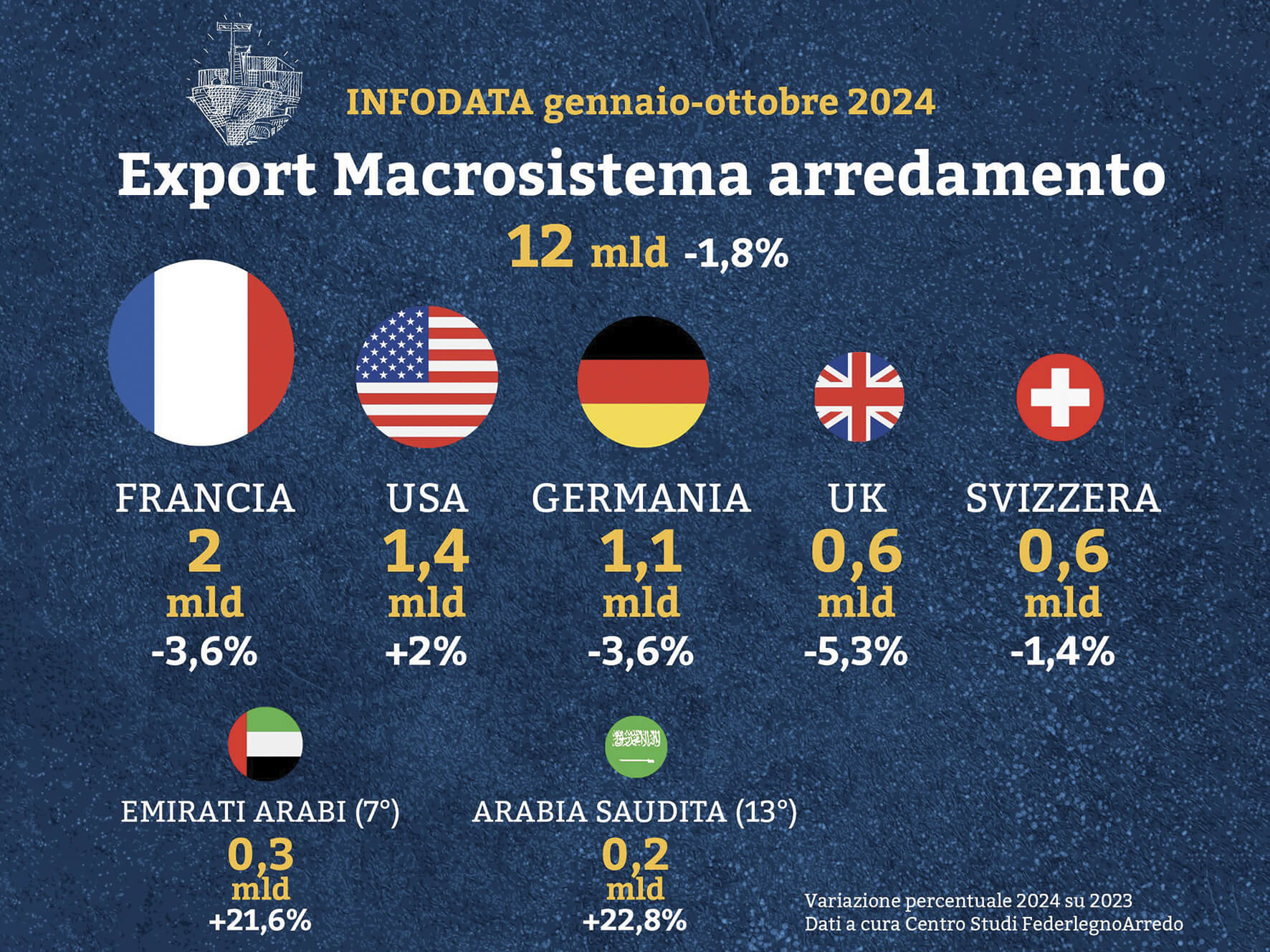

As confirmed by export data, the furniture macrosystem, declined less than the domestic market: according to the preliminary figures, the furniture macrosystem closes 2024 with about 27.5 billion euros in turnover, equal to -2.5% in 2023 when it had reached 28.2 billion euros. A decline due to a lower extent to the trend in exports (-2.1%) with a value of 14.3 billion compared to 14.7 billion in 2023, but above all to lower sales on the Italian market (-2.8%) that reaches 13.1 billion euros, compared to 13.5 in 2023. The trade balance shows 9.2 billion euros, compared to 9.6 in 2023. If 2023 closed with a -4% contraction in exports, in 2024 that decline shows less intensity (-2.1%) determined above all – as evidenced by the analysis of trade flows in the January/October 2024 period – by the contraction towards France, (-3.6%) which is still confirmed as the first market for our design with a value of 1.96 billion euros.

Heavy losses in exports to China (-17.9%), worth 313.5 million euros. However, Italy is confirmed as the first supplier for the Chinese market. Germany, the third largest market (-3.6%) is worth 1.1 billion euros. The United States, the second reference market, is stationary, recording +2% and reaching a value of 1.4 billion euros), but it could already close in the negative at the end of the year. The contraction of the furniture macrosystem is mainly contained by higher exports to the United Arab Emirates (+21.6% for 317.6 million euros), which recorded a positive trend for the fourth consecutive year, and Saudi Arabia (+22.8%), in thirteenth place, which is worth 193.5 million euros.

The wood macrosystem – excluding wood trade amounting to 3.6 billion euros – which had recorded a double-digit decline in 2023, 2024 still suffers a decrease in turnover (-5.6%), albeit more contained, standing at 20.5 billion euros. A contraction determined by the domestic market (-6.5%), which contributes more than 75% to total turnover, reaching 15.6 billion euros. Exports (24% of the total) stand at just under 5 billion euros, down 2.6% in 2023.

From the analysis of trade flows in the period January-October 2024, Germany (-11.4% to 588 million euros) and the United Kingdom (-11.3% to 452 million euros) are particularly noteworthy: the United States is growing (+9.6% to 366 million euros) but could worsen at the end of the year, while France is almost stable (-1.8% to 657 million euros), but with reasonable chances that the end of the year could be worse. The negative trend affected all systems, albeit with different variations.

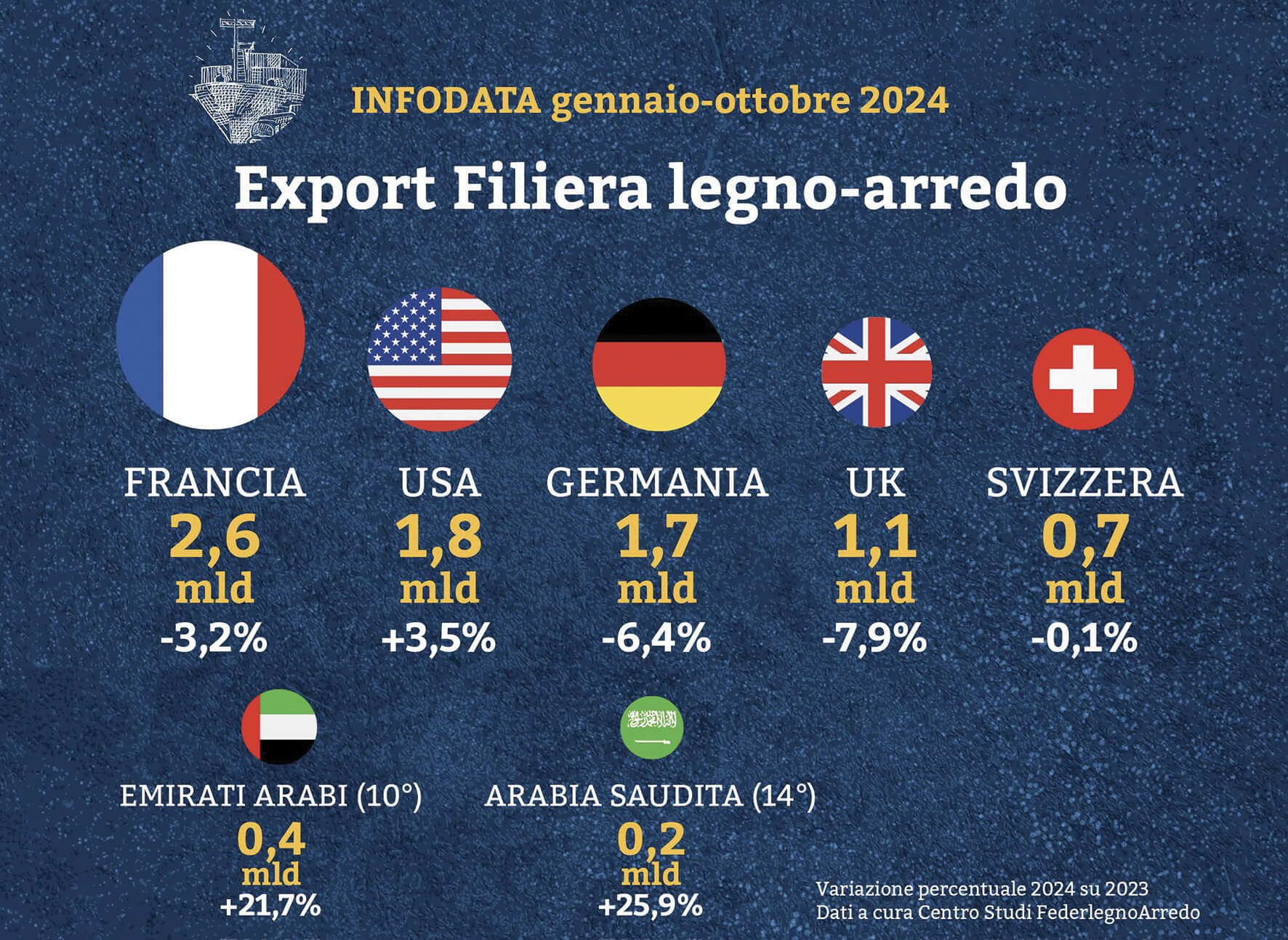

“Among the top five destinations in our supply chain,” Feltrin concludes, “it is always the USA that performs best, at least based on the analysis of trade flows for the period January-October 2024, with +3.5% for a value of almost 1.8 billion euros. At the end of the year, the situation could return to being negative or, at best, stabilize. France, the first country in the top ten, is down, recording -3.2% and worth 2.6 billion euros, while Germany with -6.4% and the United Kingdom with -7.9% underline the complexity of the moment. Spain drops to the sixth position, with a stationary trend and values similar to Switzerland, which occupies the fifth position. The United Arab Emirates is still growing with +21.7% (67 million euros more than in 2023) ranking tenth with a value of 376 million euros; Saudi Arabia indexes fourteenth with a growth of 25.9% (47.4 million euros more than in the same period of 2023) for a value of 230 million euros”.

![|COMPO ARREDO|

– Puricelli Group: when design meets sustainability –

From May 20 to 23 2025, Puricelli Group will participate at Interzum, the prestigious international trade fair dedicated to materials and technologies for design and furniture, in Cologne.

The stand will be the perfect stage to showcase its two main cores: K&B and N.EXT.

K&B is the collection dedicated to interiors, specifically designed for kitchens and bathrooms. With innovative and sustainable solutions, K&B combines design and functionality, offering durable, modern, and aesthetically appealing materials. N.EXT, instead, is the Group’s offering for exteriors. Ideal as an alternative to traditional architectural materials, N.EXT combines weather resistance with aesthetic versatility, making it the perfect choice for innovative projects with high technical value.

[Full article on our web platform]

@puricelli_group

_

#laminate #surface #sustainabilty #circularity #kitchenfurniture #bathroomfurnıture #puricelligroup #compoarredo #staffeditoriale](https://www.staffedit.it/wp-content/plugins/instagram-feed/img/placeholder.png)